Welcome to the home of Farm Financial Standards Council

2025 Annual Conference “Standing on the Shoulders of Giants”

July 23 - 25, 2025

DEADLINE to Register is July 7, 2025

Space is limited

Learn More

Conference Announcement!

Join us for our upcoming conference, “Standing on the Shoulders of Giants,” on July 23-25 in Lexington, Kentucky!

Engage with industry leaders, network with peers, and learn from esteemed speakers.

Registration NOW. We can't wait to see you there!

The Farm Financial Standards Council is dedicated to helping farmers by promoting uniform financial reporting and analysis in the ag industry. We are the definitive resource for financial guidelines that benefit farmers.

Become A corporate Partner

Click here or tap the icon above to learn more.

Become A Member

- Participate in Council Committees

- Eligibility to stand for election to the Board of Directors and/or officer positions

- Discount off published registration rate for the Annual Conference

- Automatic and complimentary updates on Financial Guidelines for Agriculture and Management Accounting Guidelines for Agriculture

Contact us

Latest News

Addendum to Farm Financial Standards Council’s Loan Assistance White Paper

Council Members Elect New Officers

Annual Conference 2024

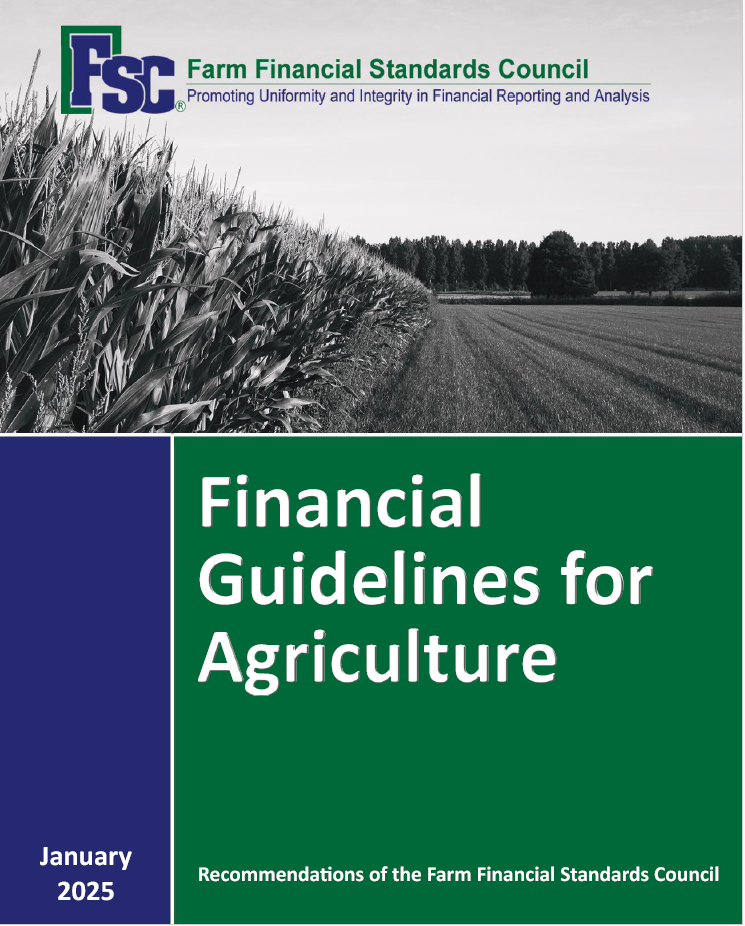

Financial Guidelines

The Financial Guidelines for Agricultural Production provides recommended standards for format and content of financial reports, recommended financial measures common to all sectors of agriculture, and example statements and measures.

Cost: $50

Management Guidelines

The Management Accounting Guidelines for Agricultural Production responds to the ever-increasing need for consistent, reliable, and accurate management information systems to support day-to-day production decisions.

Cost: $50